Macro Movers & Shakers

| Growth | Inflation | Policy | |

|---|---|---|---|

| US | • The US economy remains relatively resilient, supported by recent data and its status as a net oil exporter. • Hiring has slowed as companies focus on efficiency rather than expansion. • Consumer spending dipped temporarily, but the One, Big, Beautiful Bill Act (OBBBA) tax refunds should help support growth ahead. |

• Higher oil prices may lift inflation in the short term. • The impact is likely to be more manageable in the US than elsewhere. • Softer demand and a cooling jobs market should help keep price pressures in check. |

• The Federal Reserve (Fed) is taking a wait and see approach, as the board is divided on rates action. • The Fed has dual mandate to promote maximum employment and price stability, and could look through near term inflation caused by energy. • Keeping the job market stable remains the priority |

| Europe | • Europe is more exposed to higher energy prices and world growth than the US, which increase growth risks. • Higher energy costs are weighing on household spending and squeezing company profits. • As a result, growth remains vulnerable to further energy shocks, and outlook uncertain. |

• Energy costs are pushing up everyday living expenses. • Inflation remains elevated due to imported energy prices. • Weaker demand limits the risk of runaway inflation. |

• The market is now expecting European Central Bank (ECB) to hike interest rates 2 x this year. • Policymakers are cautious after the 2022 energy shock. • Fiscal policies expand for higher defense spending. • ECB has a primary mandate of price stability. |

| Asia | • China’s growth is stable but uneven, with a lower target of 4.5 to 5 percent reflecting a focus on sustainability rather than speed. • Domestic spending remains weak, so exports continue to play an important role in supporting growth. • Across Asia, countries will be faced with lower growth. while China/HK and Singapore offers relative stability. |

• Inflation pressures in China is welcomed to move it out of its dis-inflation regime. However, much of Asia remain relatively challenged with higher energy and food prices. • While China is less exposed to global energy shocks, higher oil and gas prices still pose risks for some industries. |

• China still has policy room to support growth if needed, including lowering borrowing costs or easing bank requirements. • Policy remains focused on long term investment in technology and productivity, rather than large scale consumer stimulus. • Across Asia, policy outlook has shifted, ready to fight higher energy and food prices |

| Japan | • Japan’s outlook has become more uncertain as higher oil prices raise costs across the economy. • Elevated energy costs could weigh on business profits and slow growth in the near term. • Over time, continued government spending is expected to help support economic activity. |

• Higher oil prices are raising inflation risks through energy and import costs. • Ongoing government spending is likely to add some upward pressure on prices over time. • Overall, inflation is expected to trend higher, but not sharply. |

• Despite a weak yen, uncertainty favors caution. • The central bank is more likely to keep rates on hold in the near term with an upward bias. |

| RISKS |

|---|

| • Oil prices could stay high if conflicts in the Middle East disrupt supply, putting pressure on inflation and growth. • Ongoing inflation concerns and questions around central banks actions may lead to more interest rate swings and higher yields. • Further weakness in Markets could be triggered by rerating of valuations across AI-tech companies if earnings growth slows |

Sensible Considerations

Valuation based on Price-to book ratio.

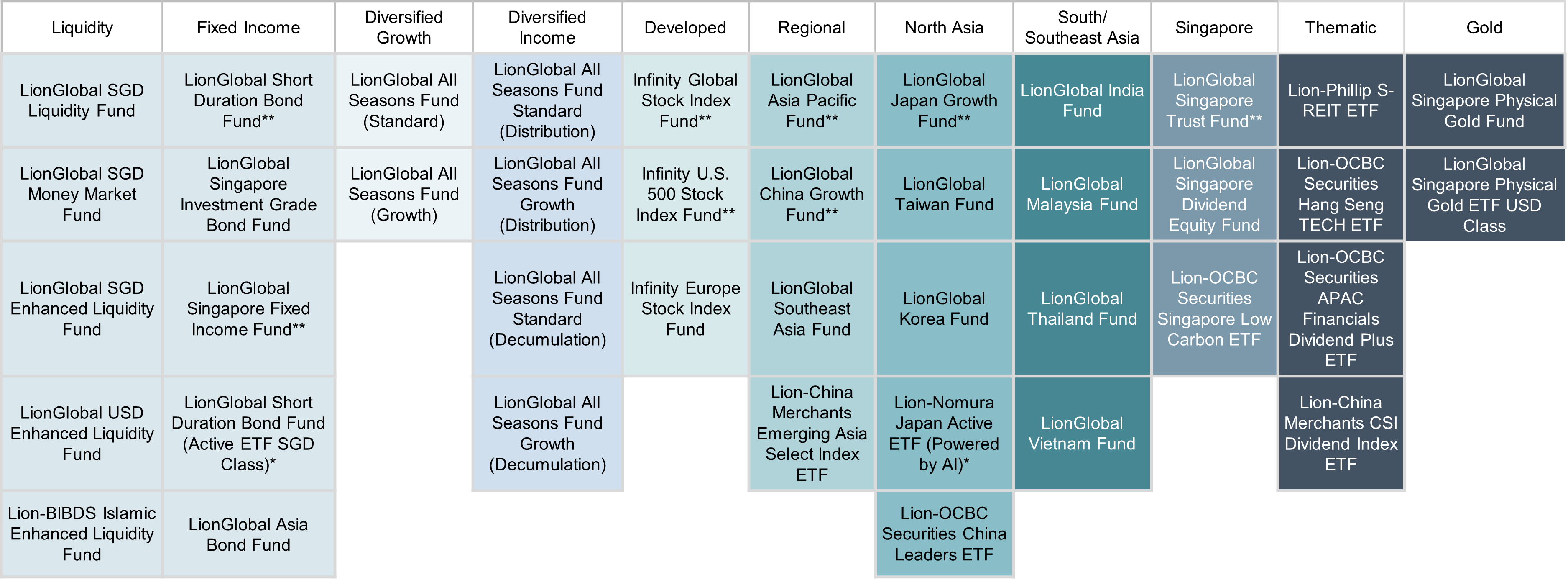

At a Glance | General Product Suite

*This is an actively managed ETF

**CPFIS Funds: LionGlobal Short Duration Bond Fund Class A SGD (Dist), LionGlobal Singapore Fixed Income Investment Class A SGD, Infinity Global Stock Index Fund SGD, Infinity Global Stock Index Fund Class C SGD, Infinity U.S. 500 Stock Index Fund SGD, Infinity U.S 500 Stock Index Fund Class C SGD, LionGlobal Asia Pacific Fund SGD, LionGlobal China Growth Fund SGD, LionGlobal Japan Growth Fund SGD, LionGlobal Japan Growth Fund SGD-Hedged and LionGlobal Singapore Trust Fund SGD.

All data are sourced from Lion Global Investors as of 31 March 2026, unless otherwise stated.