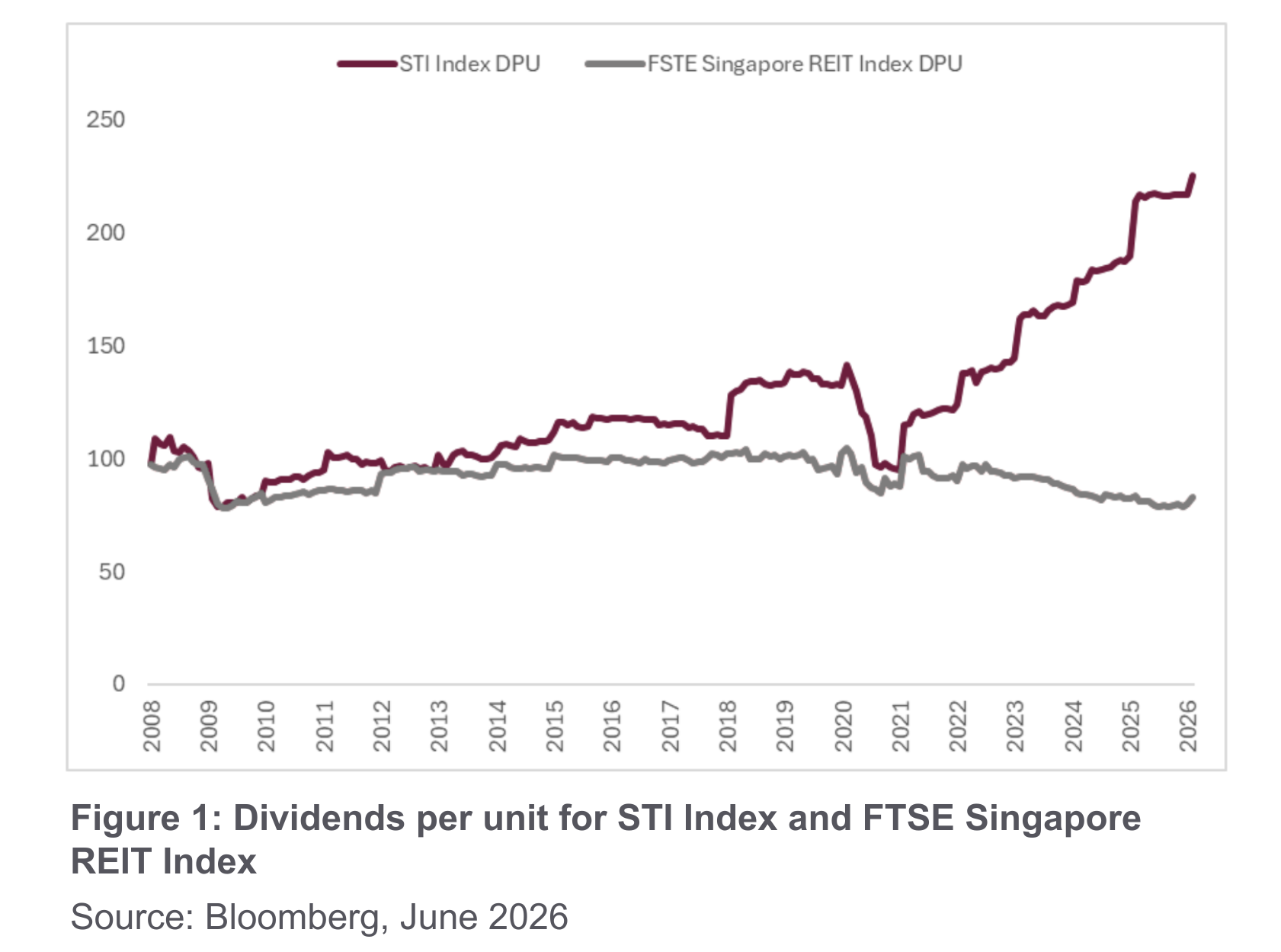

The Singapore Equity market is well-established as a high dividend equity market. Whilst dividend per share have been stable post 2008 Great Financial Crisis (GFC), dividends per share have notably increased in the period after the 2020 COVID (see Figure 1 below).

Importantly, whilst dividends offered by Real Estate Investment Trust (REITs) remain stable, major sectors have been increasing dividends, such as the Financials, Industrials and Telecommunications sectors that contribute more than half of the benchmark Singapore Straits Times Index (STI). This increase is driven by a combination of the positive signalling effect from the Temasek Strategic Review of its portfolio investments in 2021 to improve capital efficiency, as well as improving earnings sustainability across these major sectors.

Therefore, the Singapore Equity market is undergoing a paradigm shift, from one of stable dividends to one of growing dividends, offering investors both dividend yield and capital appreciation.

Singapore as a Global Safe‑Haven Growth Platform

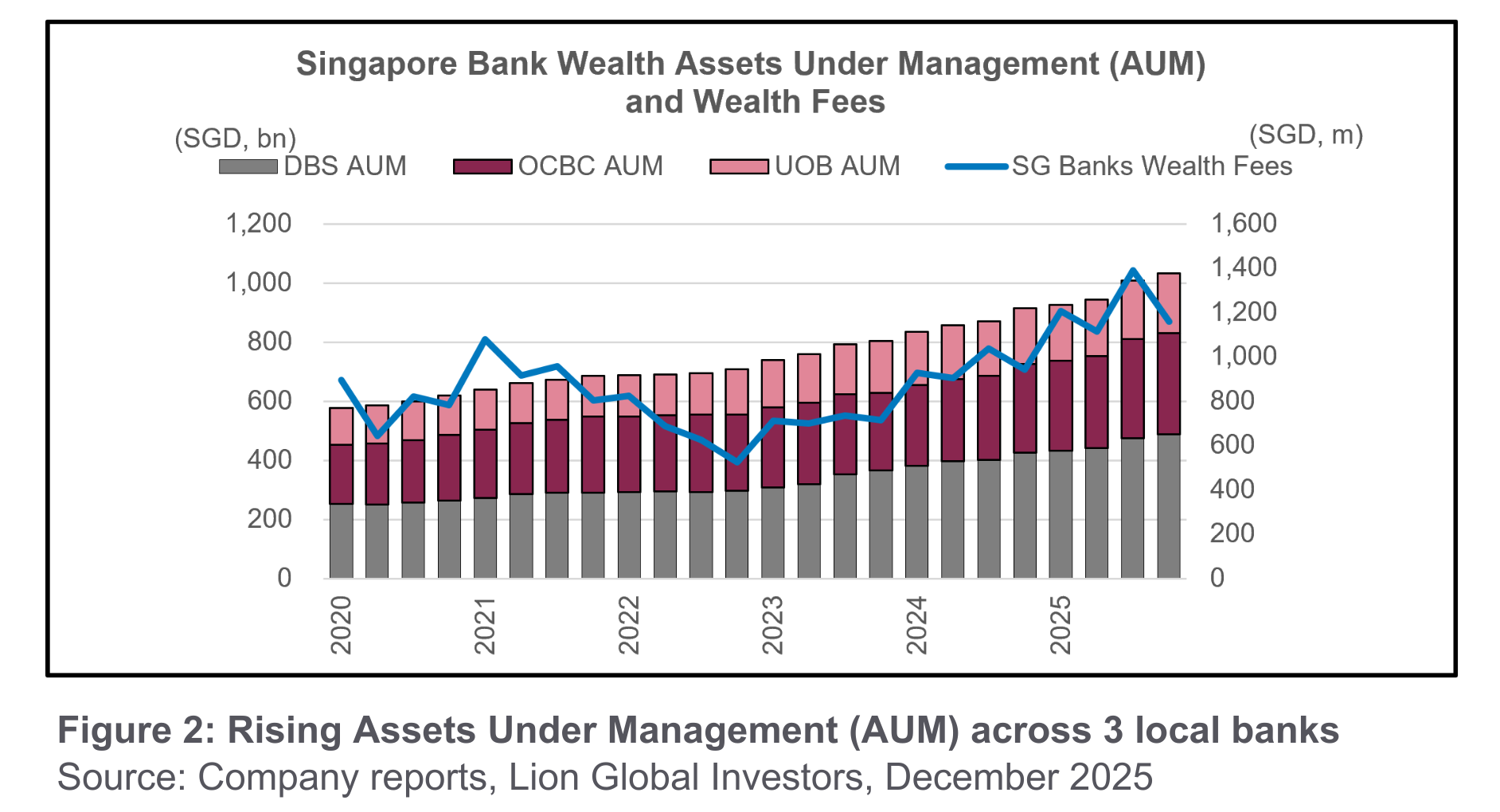

A major driver of STI Index strength has been the Financials sector. Singapore’s safe‑haven status has led to rising assets under management across the three local banks, supporting solid earnings growth.

The strong growth in the wealth management businesses enables Singapore banks to support a higher dividend payout ratio, enabling dividends per share to increase. This is because unlike the traditional lending business, banks are not required to set aside a capital buffer for the wealth management business. Therefore, fee income from the wealth management business can more efficiently be translated into dividend payouts for shareholders.

Given continued geopolitical tensions worldwide, Singapore’s appeal as a safe haven should remain intact, or even strengthen. This is likely to maintain the strong momentum of the Singapore banks’ wealth management businesses and dividend payout capacity.

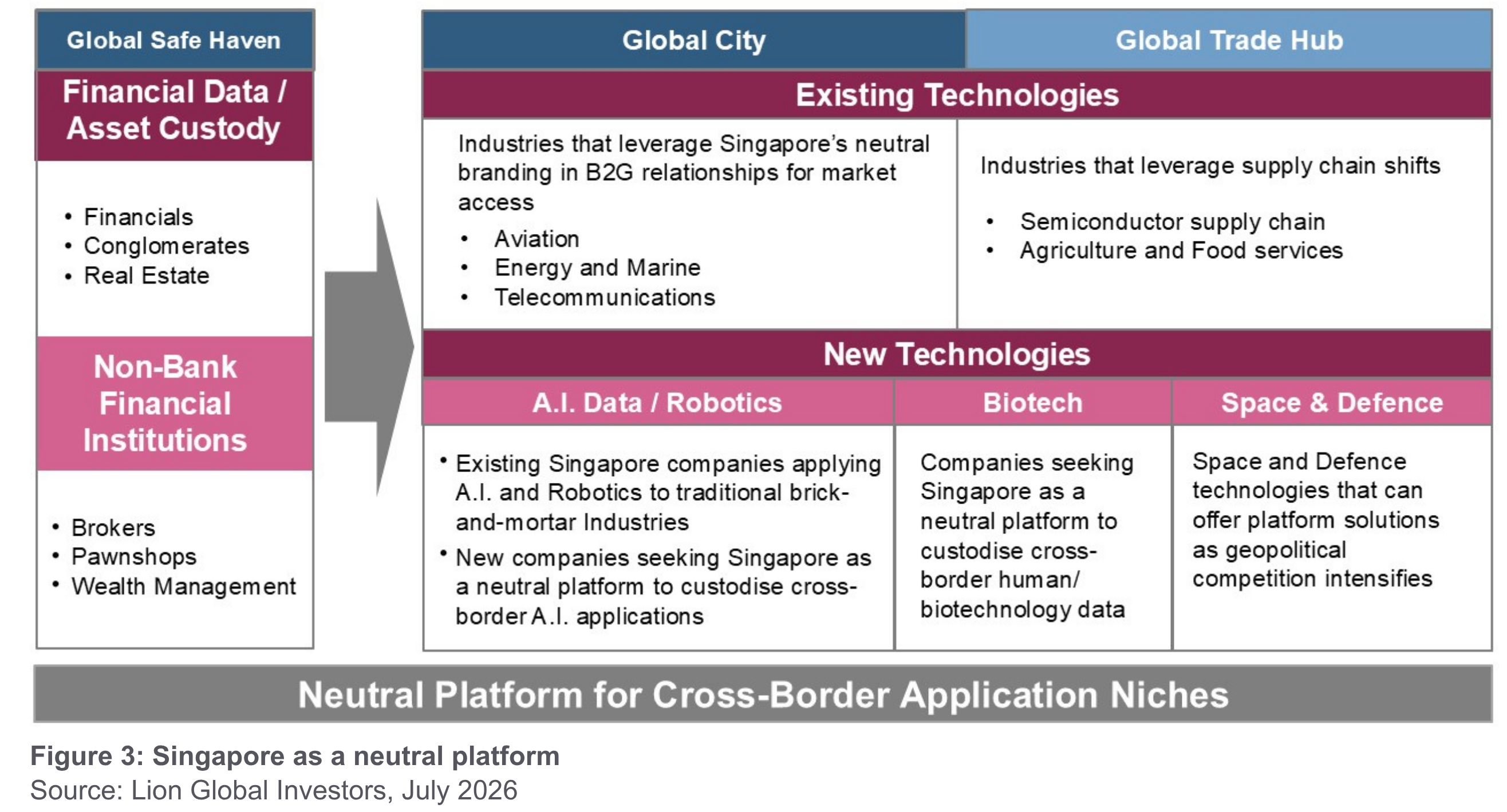

Broadening the Investible Universe: A Neutral Export Platform

Singapore’s strong track record in the Financials sector underscores its reputation as a neutral, trusted, and stable hub. Building on this, the equity market can further develop growth themes tied to Singapore’s role as a geopolitically neutral platform for cross‑border export activities.

Existing export‑related sectors within the STI, including Aviation, Energy & Marine, and Telecommunication, already leverage Singapore’s brand strength in Business‑to‑Government (B2G) markets.

Looking ahead, emerging industries such as artificial intelligence, biotechnology, and space technology offer new opportunities. These areas are often subject to geopolitical sensitivities, and Singapore’s neutrality, positions it well as a launchpad for companies seeking cross‑regional expansion. This could encourage more Asian companies to establish their international headquarters here and list on the Singapore Exchange, widening the pipeline of future growth sectors, particularly within the Small and Mid-Cap (SMID) space.

Sustainability of the Singapore Equity Market

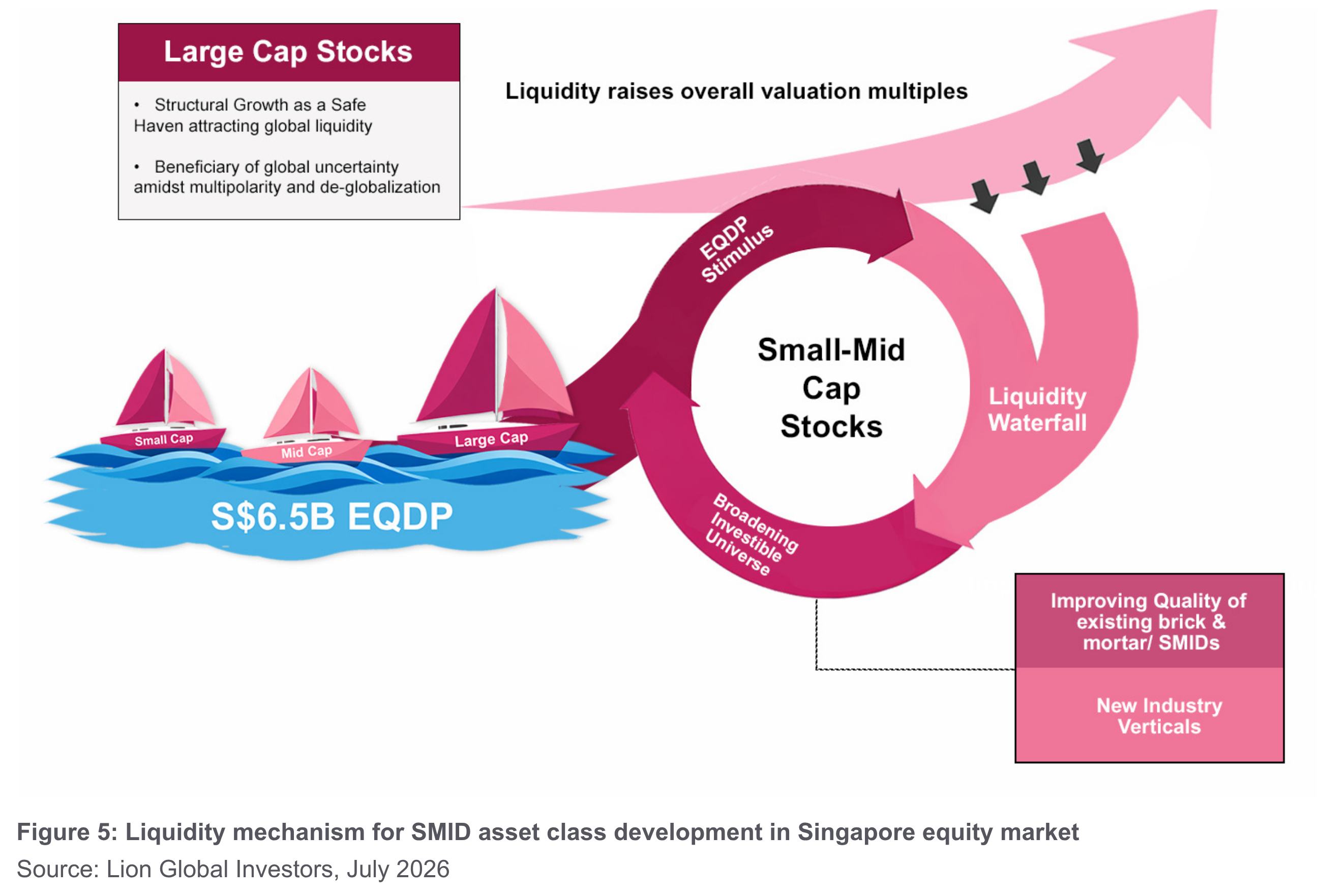

Recently, the Monetary Authority of Singapore’s (MAS) Equity Market Development Programme (EQDP), with S$6.5 billion committed to date, of which S$3.95 billion has been announced as at 19 November 2025, has further boosted attention and activity in local equities.

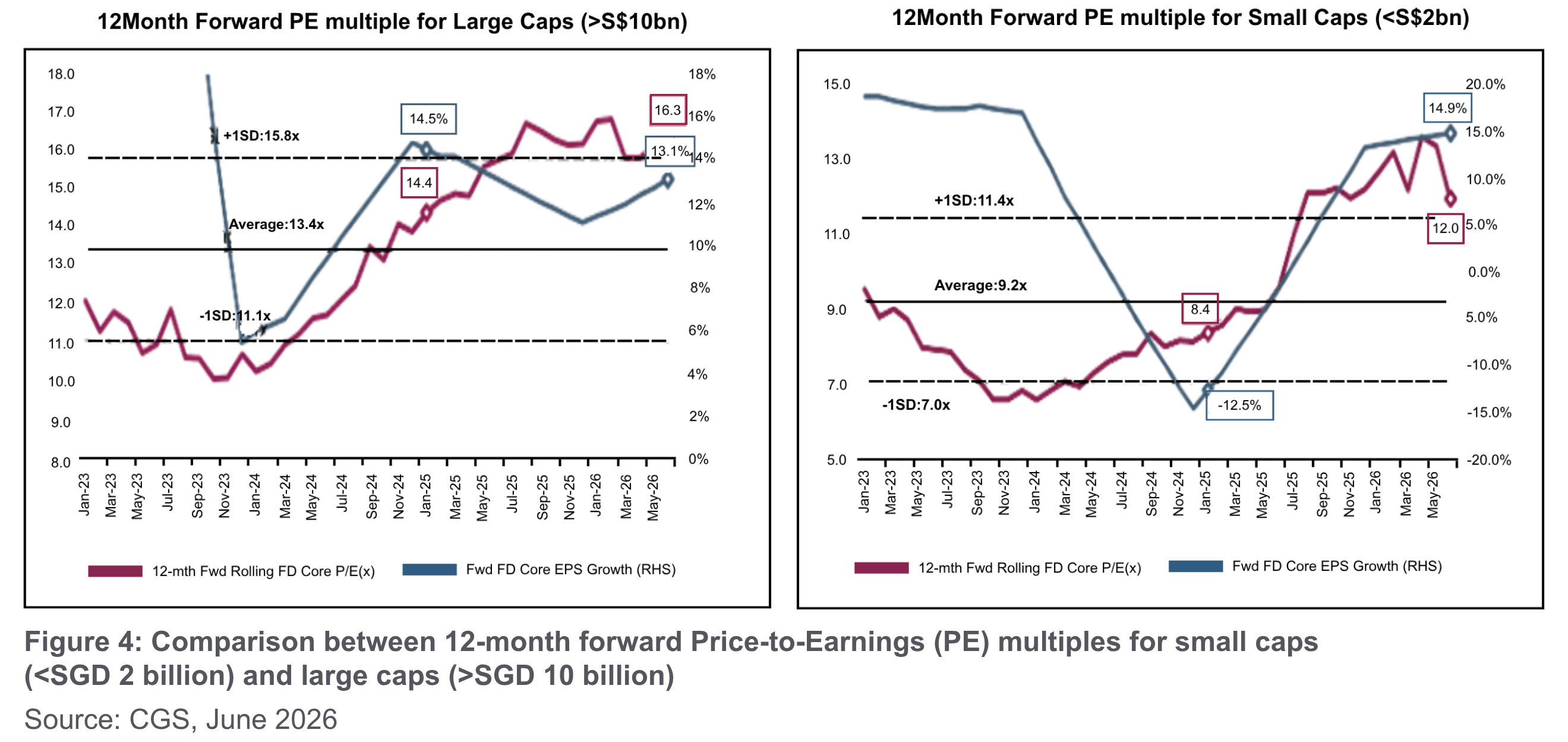

As a result, small-cap stocks in the Singapore market have performed well since 2025. Whilst valuation multiples have re-rated from below 10x Price-To-Earnings (PE) to current levels of 12x PE for small-caps, valuations still remain attractive relative to growth expectations of around 15% for this asset class. This compares favourably with large caps, which trade at a higher 16x PE but with lower growth expectations of 13%. Therefore, the overall Singapore Equity market has room to continue to evolve in terms of price discovery and valuation expansion.

With this support in place, the key question now is: How sustainable is the Singapore market’s strong performance beyond the EQDP stimulus?

In terms of policy, revisions to the Central Provident Fund (CPF) scheme in 2028 could pave the way for greater allocation to equities, including Singapore equities. This presents a runway of potential liquidity to support the continued revitalisation of the Small-Mid cap market beyond the EQDP programme, which is expected to be deployed through 2027.

Beyond government policy, the STI Index is also benefiting from Singapore’s growing role as a global safe haven amid prolonged geopolitical uncertainty, a trend that is likely to persist well beyond 2026.

This structural tailwind is creating a significant opportunity. Rising global capital flows seeking stability may continue to drive a re‑rating of Singapore equities. As liquidity increases, more growth‑oriented small and mid‑cap companies may be attracted to list on the Singapore Exchange, expanding the investible universe and creating a virtuous cycle of market development.

The chart below outlines a framework explaining the liquidity mechanism that can fuel the development of the SMID asset class in the Singapore equity market:

Conclusion

The Singapore equity market is at an important inflection point, supported by multiple structural drivers:

Attractive dividend yields with improving dividend per share.

Safe-haven inflows driven by ongoing global geopolitical uncertainty.

Policy support through the MAS EQDP, which helps catalyse new growth themes and broaden the SMID opportunity set.

In short, Singapore offers investors a compelling combination of strong dividends and long-term structural growth. The outlook for the market remains robust as these drivers continue to reinforce one another.

All data are sourced from Lion Global Investors and Bloomberg as at 1 July 2026 unless otherwise stated.