For years, headlines have painted a bleak picture of China’s economic outlook - property market woes, manufacturing overcapacity, and geopolitical uncertainty. Yet beneath the noise, a quiet rally has been building. Chinese equities climbed 20% in 2024 and surged 34% Year-to-Date (YTD) by the end of September 20251, revealing one of the most compelling investment stories in recent memory.

Figure 1: 5-Year Performance of MSCI Golden Dragon Index (USD Terms)

MSCI Golden Dragon Index was up by 20% in 2024 and 34% as of end September 2025 YTD

The Real Story

While the property sector remains challenging, the broader investment narrative is shifting. Three structural forces are reshaping China’s capital markets:

Policy Priority: Since September 2024, the Chinese government has been promoting sustainable growth for its equity market2. Interest rate cuts, lower bank reserve requirements, and liquidity backstops have created a more supportive environment for investors.

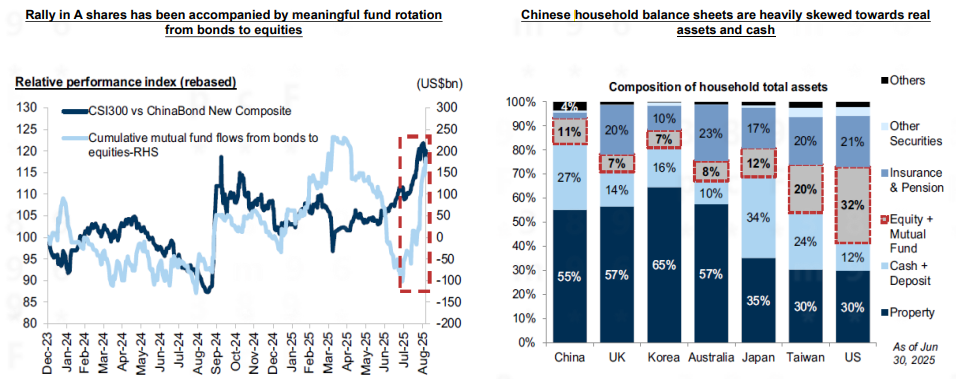

Household Reallocation Potential: With government bond yields at just 1.9% and property losing its appeal, Chinese households are poised to reallocate trillions into equities. Currently, only 11% of household assets are in equities, compared to 32% in the U.S.3 - a gap that signals immense upside.

Figure 2: 5-Year Performance of China 10-Year Government Bond Yield (USD Terms)

Low 10-Year government yield of 1.9% continues to drive investors towards the equities market

Source: Bloomberg, September 2025

Figure 3: Rally in A shares has been accompanied by meaningful fund rotation from bonds to equities & Chinese household balance sheets are heavily skewed towards real assets and cash

Strategic Fiscal Firepower4: China’s response to trade tensions has been measured but deliberate. Rather than reacting to short-term volatility, policymakers are prepared to deploy targeted stimulus if economic data weakens, ensuring resilience in the face of global uncertainty.

Five Themes Powering China's Investment Revival

Investors are increasingly looking to China for exposure to transformative sectors. Five themes stand out:

2. Chinese Intellectual Property: Chinese intellectual properties, such as Labubu, are expanding rapidly in global markets. China is also a major player in the global mobile gaming market creating successful titles such as PUBG mobile and Genshin Impact. In the years to come, we believe that Chinese companies will continue to create Chinese intellectual property with increasing global appeal.

3. Electric Vehicles and Autonomous Driving: China has 50% EV penetration - the highest globally5. China is dominant in the LiDAR market which is essential for self-driving technology by creating high resolution maps. Chinese LiDAR manufacturers are driving down LiDAR costs from USD$20,000 to USD$200 per unit6, enabling mass adoption.

4. Humanoid Robots: With aging populations and labour shortages, the humanoid robot market could reach USD$1.4 to USD$1.7 trillion by 20507. The humanoid robot supply chain will be predominantly Greater China-based.

5. Industrial capabilities: Chinese construction machinery, batteries, and energy storage systems are also steadily gaining global market share, driven by superior technology at competitive prices.

A Market Reawakens

Figure 4: Market Equities Benchmark Index

For those seeking exposure to innovation, scale, and long-term growth, China’s equity market offers a compelling case for inclusion in diversified portfolios.

2Source: Xinhua, HSBC, September 2025

4Source: Citi Research, September 2025

5Source: CAICV & Foresight Industry Research Institute, 2024

6Source: Dewesoft, Hesai, September 2025

7Source: UBS, 2025

All data are sourced from Lion Global Investors and Bloomberg as at October 2025 unless otherwise stated.