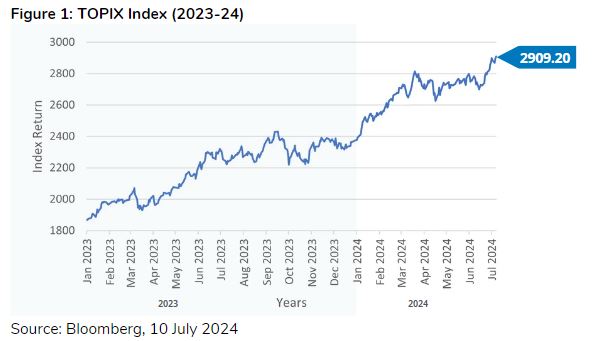

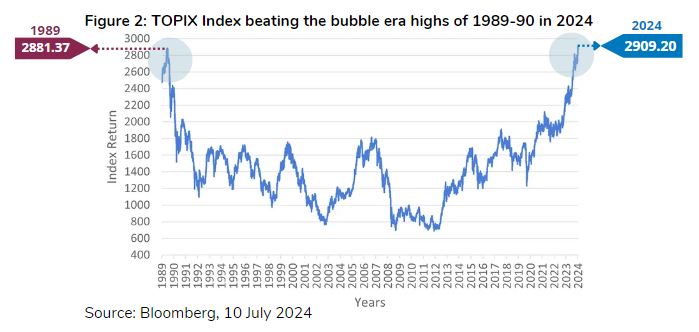

Since our previous update on the Japan market in April 2023, events have turned out much as expected and the Japan stock market has delivered stellar returns through this period, with the TOPIX Total Return Index giving 28.3% return in 2023 and another 20.1% return in 1H2024 in Japanese Yen terms1 . Both the broad market index TOPIX and well-known Nikkei 225 achieved new historical record highs in early July 2024, beating the bubble era highs of 1989-901.

To recap the events and our expectations in April 2023, the Tokyo Stock Exchange requested companies to take steps to improve their capital efficiency and corporate value. This led to the majority of corporate management in Japan delivering much improved corporate governance and shareholder returns in 2023 and so far in 2024, with record levels of dividends and share buyback announcements made in the fiscal year ended in March 2024 and a new quarterly record value of share buyback announcements expected for the first quarter of the new fiscal year. At the same time, the rapidly improving inflation and wage hike cycle has led the Bank of Japan (BOJ) to remove its ultra-easy monetary policies of Negative Interest Rate Policy (NIRP) and Yield Curve Control (YCC) in March 2024, and the BOJ is now preparing to reduce its government bond purchases and lift interest rates further. Investors have responded positively to the change in both management attitudes and the macro environment, pushing the stock market to new record levels.

So, what can we look forward to from now? The simple answer is “more of the same”.

Early Stages of Corporate Governance Reforms

Japanese companies are in the early stages of corporate governance reforms which will lead to better shareholder returns. Together with proxy voting advisors, many institutional investors in Japan have started to tighten their voting policies to hold top company executives responsible to deliver higher returns on capital, accelerate unwinding of crossholdings and reduce holdings of excess cash. Activist investors have further increased their presence and shareholder proposals have further ratcheted up in 2024. As a result, approval rates for top executives have declined in general during the 2024 Annual General Meetings (AGM). While the approval rates have not declined to alarming levels for many companies, they serve as continued pressure to keep improving returns for shareholders or face further scrutiny in the next AGM. At the same time, another category of investors has come into play. These are new individual investors who have been incentivized by the enhanced NISA program, which allows tax-free stock investments for Japanese retail investors. Many of these investors focus on stable and rising dividends, leading many companies to tweak their shareholder return policies to focus on keeping dividends stable and rising continuously. Such return policies help reduce market volatility in times when earnings are uncertain.

Deflation to Inflation

The other area of change is Japan’s shift from deflation to inflation. The 2024 spring wage hike outcome recently announced was a base pay rise of 3.56% and headline wage increase of +5.10%, accelerating sharply from the 2023 hikes of 2.12% and 3.58% respectively2 . These are figures not seen since the bubble era in the early 1990s. The accelerating wage hikes together with inflation that is sustaining at above 2%3, is expected to bring about a change in attitudes by both consumers and corporates’ spending. We have already seen a consistent rise in capital expenditure by corporates since 2022, brought about by improving profitability, inflationary outlook and tightening labour shortage. We expect consumers to join the increase in spending as well as shift their large cash holdings into higher yielding assets such as stocks where companies are raising dividends and bonds where the Bank of Japan (BOJ) is expected to further lift interest rates.

Structural Changes in Corporate Governance

Unlike the stock market bubble in 1990, the new record high market levels in Japan recently achieved were backed by structural changes in corporate governance and the economic environment, leading to re-appraisal by global investors. As Japan is only in the early stage of these structural changes, we expect such changes to continue in the foreseeable future and the re-rating of the Japan stock market by global and domestic investors to continue in tandem.

For the full list of awards, please refer to www.lionglobalinvestors.com

Our LionGlobal Japan Growth Fund and LionGlobal Japan Fund both seek to participate in the ongoing corporate reforms and improving shareholder returns at Japanese corporates. In particular, we focus on companies with strong global competitiveness and can ride on structural growth trends and grow through value-added products. In addition, we will focus on companies that have the capacity to improve on shareholder returns and companies that will benefit from the recovery of pricing power in Japan.

All data are sourced from Lion Global Investors and Bloomberg as at 8 July 2024 unless otherwise stated.

1Source: Bloomberg, Tokyo Stock Exchange, Nikkei, as of 8 July 2024

2Source: Japanese Trade Union Confederation (Rengo), as of 3 July 2024

3Source: Bloomberg, Ministry of Internal Affairs and Communications, as of 8 July 2024